Identify & Configure Leases

- 11 Oct 2022

- 2 Minutes to read

-

Contributors

-

Print

-

DarkLight

Identify & Configure Leases

- Updated on 11 Oct 2022

- 2 Minutes to read

-

Contributors

-

Print

-

DarkLight

Article Summary

Share feedback

Thanks for sharing your feedback!

Overview

Background for Identifying Contracts with Lease and Non-Lease Components:

The first requirement in using NetLease is to identify what leases are as defined under the new accounting standards. Although this may seem intuitive, determining what constitutes a lease may be less than straightforward. The general approach is to (1) identify contracts that contain a lease, and (2) determine the various components of the contract to segregate between the lease and non-lease components.

NetLease is primarily focused on the recording and compliance for the lease components of a contract; however, we also provide tools to support the tracking and management of non-lease components of a contract. When establishing a lease in NetLease, it is important to segregate and carry forward only the lease components to the primary header and payment fields for the lease.

For more comprehensive support, we recommend partnering with an established accounting and consulting firm experienced in adoption and interpretation of ASC 842 and IFRS 16. We would be happy to provide recommendations.

Lease Definitions under both Standards:

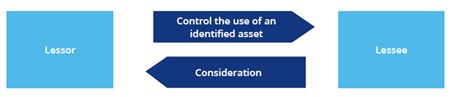

ASC 842-10-15-3 defines a lease as follows:

A contract — or part of a contract — in which a supplier conveys to a customer “the right to control the use of identified [PP&E / Asset] for a period of time in exchange for consideration.”

IFRS 16:Appendix A similarly defines a lease as follows:

A contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration

The relationship between a lessor and lessee is illustrated below (from Deloitte’s ASC 842 Roadmap)

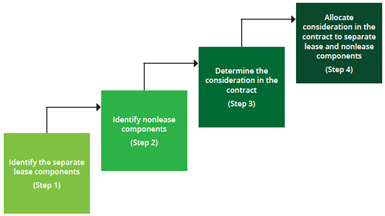

Lease and Non-Lease Components:

Many contracts may contain both Lease and Non-Lease components (e.g., rent of office space plus monthly CAM charges). Deloitte provides the following 4-step process to separate lease and non-lease components:

Note that the Lease components you identify in a contract are the amounts that should be carried forward and set up specifically within NetLease in the payment schedules, while additional actual and/or estimated non-lease expenses can be noted under the Documents tab at the bottom of a lease record.

NOTE: Both ASC 842 and IFRS 16 allow a practical expedient to not separate components. The FASB did note, however, that it would not expect lessees (even though allowed) to elect this expedient when non-lease components are significant.

ASC 842: As a practical expedient, a lessee may, as an accounting policy election by class of underlying asset, choose not to separate non-lease components from lease components and instead to account for each separate lease component and the non-lease components associated with that lease component as a single lease component [ASC 842-10-15-37]

IFRS 16: As a practical expedient, a lessee may elect not to separate non-lease components from lease components, and instead account for each lease component and any associated non-lease components as a single lease component. This election should be made by class of underlying asset [IFRS 16:15]

Was this article helpful?